Signed Directed Graphs for analyzing systemic risk in financial networkProcess Systems Engineering - SDG Model - Systemic Risk - Financial Networks

Explanation

Simulation

Contact

Flowsheet

The recent financial crisis, and the ensuing sovereign debt crisis, once again highlighted that understanding the potential instabilities in the financial system is of great societal value. Financial instability typically results from positive feedback loops intrinsic to the operation of the financial system. The challenging task of identifying, modeling and analyzing the causes and effects of such feedback loops requires a proper systems engineering perspective that is lacking in the remedies proposed in recent literature.

We propose that signed directed graphs (SDG), a modeling methodology extensively used in process systems engineering, is an appropriate framework to address this challenge. The SDG framework is able to represent and reveal information missed by more traditional network models of financial system. This framework adds crucial information to the edges in a network in terms of the direction of flows, and relationship between the variables associated with the nodes at the two ends of a directed edge; thereby providing a framework for systematically analyzing the potential hazards and instabilities in the system.

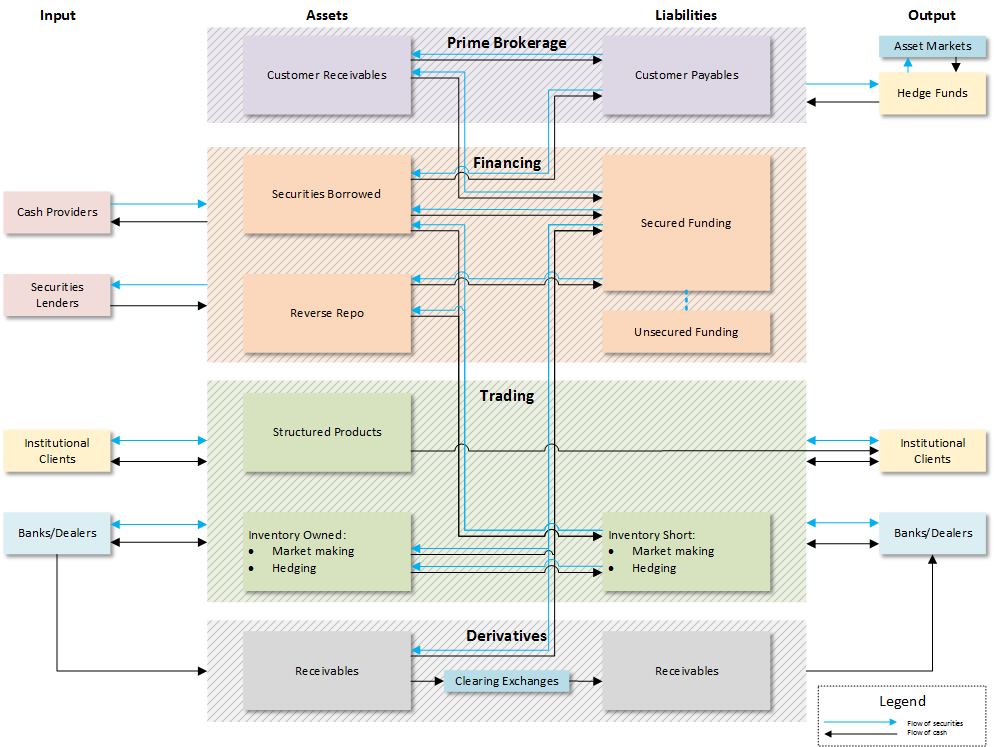

For the sake of simplicity, to demonstrate the process systems engineering inspired modeling framework, we now consider a simplified version of the reality and focus only on two types of Bank/Dealer activities shown in the first figure:

1. Funding and securities lending: The Bank/Dealer goes to sources of funding such as money market funds through the repo market, and to security lenders, such as pension funds and asset manage- ment firms through their custodian banks.

2. Providing liquidity as a market maker: The Bank/Dealer goes to the asset markets, to institutions that hold assets, and to other market makers to acquire positions in the securities that the clients demand. This function also includes securitization taking securities and restructuring them. This involves liquidity and risk transformations.

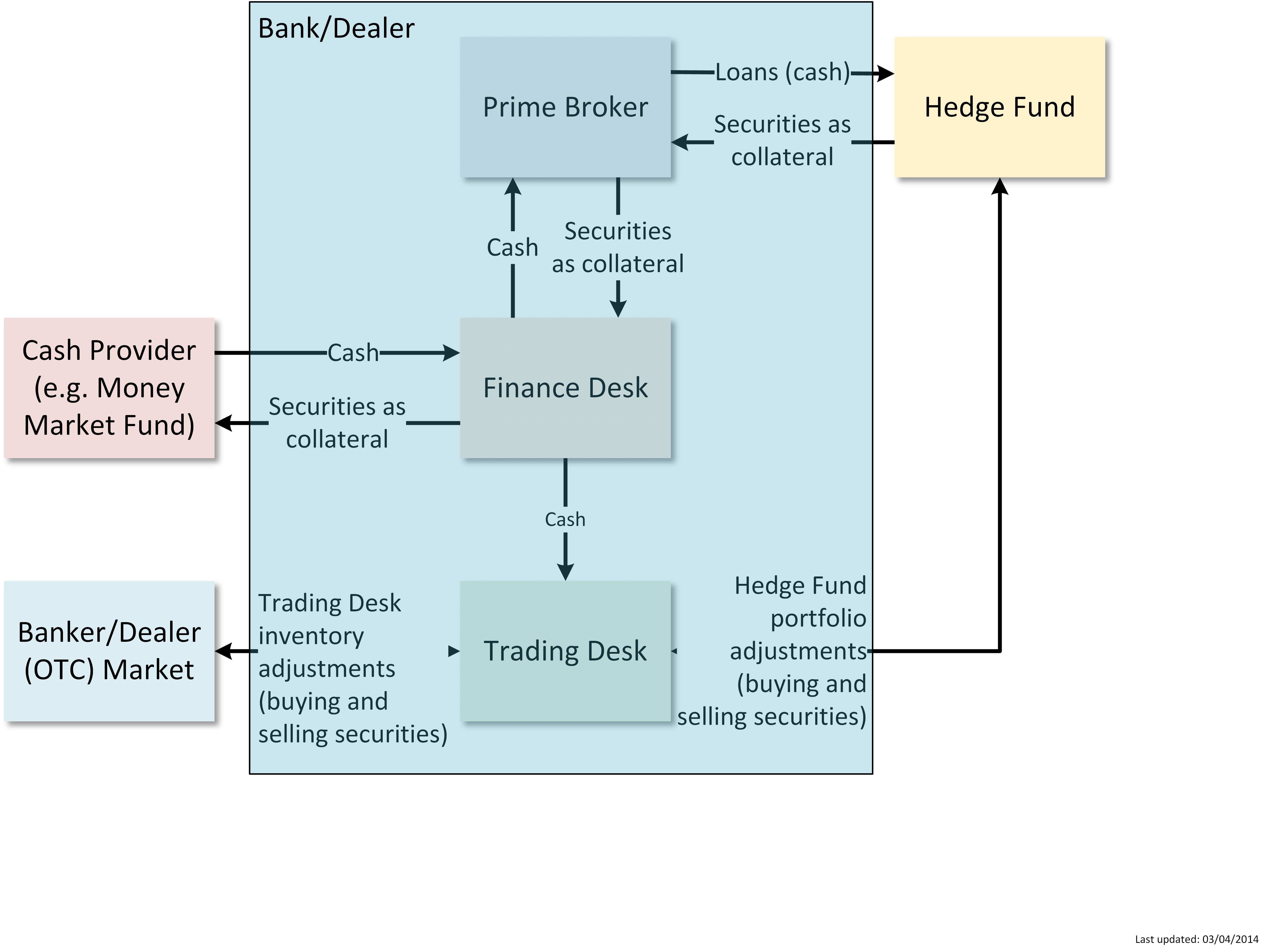

The functions we show within the Bank/Dealer include the Prime Broker, which lends cash to hedge funds in order for the hedge funds to buy securities on mar- gin; the Financing Desk, which borrows cash with high quality securities used as collateral; and the Trading Desk, which manages inventory in its market making activities that it finances through the Financing Desk. The Bank/Dealer interacts with Cash Providers, such as money market funds, pension funds, and insurance companies; other Banks/Dealers through the over-the-counter market, which is the market for the Bank/Dealer to acquire or lay off inventory; and the Hedge Funds, which, as noted above, seek leverage and securities from Prime Brokers to support their long/short trading posi- tions. The Hedge Funds also represent the wider swath of institutional customers that use the Bank/Dealer's market making function, ranging from asset managers and hedge funds to pension funds, sovereign wealth funds, and insurance companies.

The interactions between the Bank/Dealer's functional areas create various financial transformations. The Financing Desk takes short-term loans from the Cash Providers and passes them through to clients that have lower credit standing, often as longer-term loans. In doing this, the Bank/Dealer is engaging in both a maturity and a credit transformation. The Trading Desk inventories securities until it can either lay it off based on the demand of another client or to the over-the-counter market. In doing this, it provides a liquidity transformation.

The network for the Bank/Dealer is more interconnected than that of a chemical plant, because some clients, i.e., nodes that receive the output from a Bank/Dealer, are also sources of inputs. A Hedge Fund that is borrowing in order to buy securities might also be lending other securities. A pension fund that is providing funding might also be using the Bank/Dealer for market making. Hedge Funds and related institutional investors are on both sides of the production in that they are both buyers and sellers of securities, and in that sense provide inputs as well as output in market making.

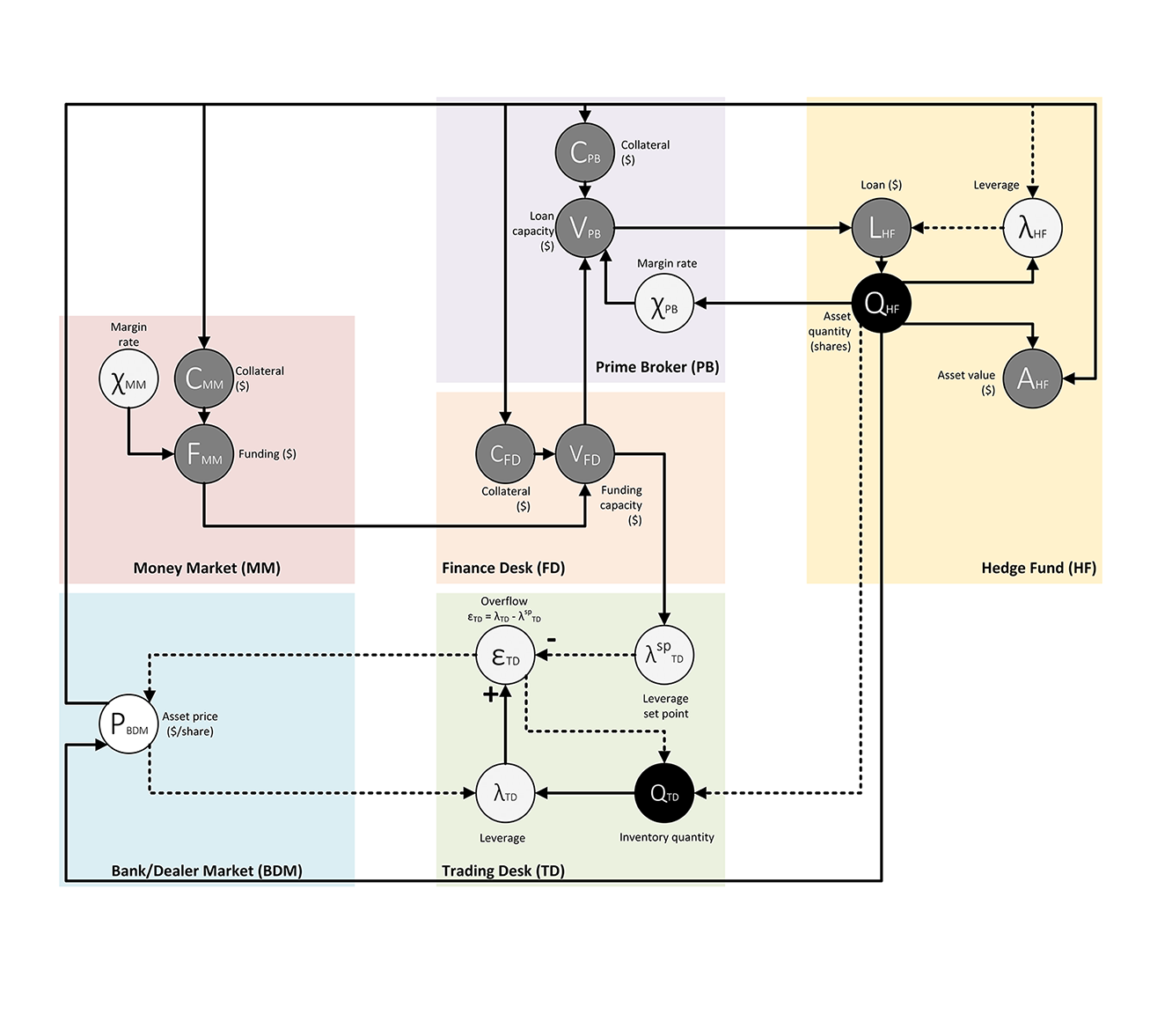

For simplicity, we consider a system with a single market asset (e.g., a stock or a bond). Its price is represented by the node PBDM, and this price level in uences, and is in uenced by the rest of the system. Quantities of the asset QHF and QTD are held by the Hedge Fund and Trading Desk, respectively. These units need funding to finance their asset holdings; this funding is provided by the Money Market, the Prime Broker, and the Finance Desk. In each case, funding availability depends on the unit's collateral level, and collateral is held in the form of the market asset. Thus, changes in the market price changes the value of the collateral, which in turn changes the level of funding available. A margin rate controls the ratio of funding capacity to collateral at the Money Market and the Prime Broker; a leverage target controls the level of borrowing relative to asset holdings at the Hedge Fund and the Trading Desk. More specifically, the Hedge Fund determines its dollar borrowing based on the availability of loans that are provided through the Prime Broker and a comparison of its assets to its target leverage ratio, lambda. The Prime Broker's lending is determined by the Bank/Dealer's Financing Desk and by the Prime Broker's margin rate, chi.

The Trading Desk provides a market making function; it stands ready to take on any quantity sent its way by the hedge fund. This increases its inventory of shares, and when this inventory becomes too large relative to a set point, it opens the over ow control to pass shares through to the market, dropping the price as a result. The Trad- ing Desk's market making function distinguishes its control mechanism from that of the Hedge Fund. As with the hedge fund, the Trading Desk depends on the Financing Desk to fund its inventory, and a drop in funding might force the Trading Desk to release more shares into the Bank/Dealer Market.

The Money Market provides funding for both the Hedge Fund and the Trading Desk through the Finance Desk; and it is changes in the funding of the Funding Desk that lead to changes in the quantity held by the Hedge Fund and the Trading Unit, ultimately changing the price.

The entire system is driven by, and feeds back into, the prices that are set in the Bank/Dealer Market. These prices are determined by the actions of the Trading Desk and the Hedge Fund, and determine the collateral value that helps drive the willingness of the various agents along the path to provide funding.

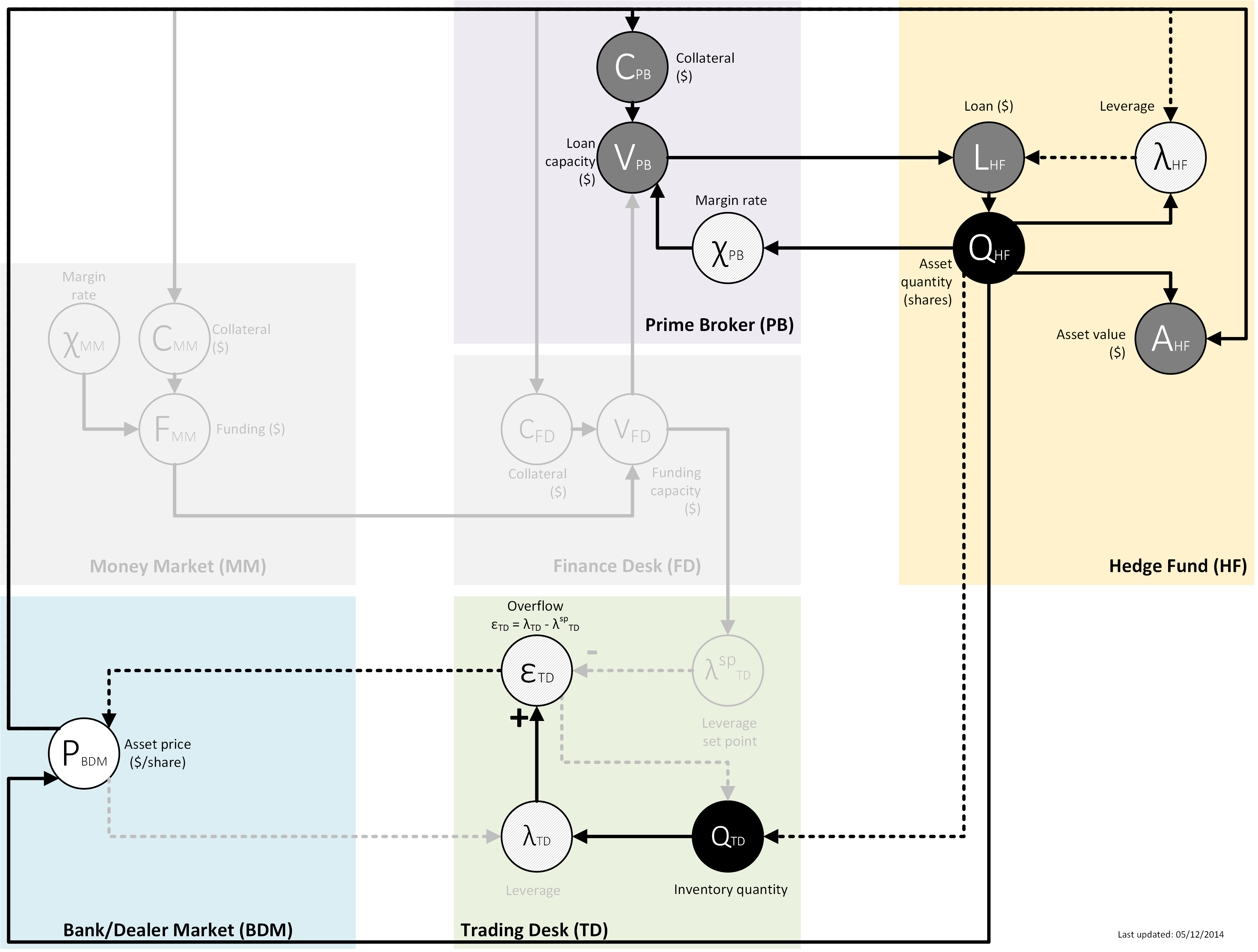

This figure shows a segment of the SDG model of the second figure that focuses on the interaction of the Hedge Fund with the Bank/Dealer's Prime Broker. The fire sale occurs when there is a disruption to the system that forces a hedge fund to sell positions. As shown in the figure of SDG model, this disruption can occur through three channels: a price drop and resulting drop in asset value, an increase in the margin rate that leads to a margin call from the Prime Broker, or a drop in the loan capacity of the Prime Broker. As the Hedge Fund reduces its assets, prices drop, again, leading to a second (and subsequent) round of feedback making the situation worse in every subsequent iteration.

The fire sale is best depicted by the two loops. The first of these loops shows a price shock increasing the leverage of the Hedge Fund. The Hedge Fund then reduces its holdings in order to reduce its leverage, and this drops prices. The second loop has the same effect, drop in prices increases leverage, which in turn leads to a drop in the quantity held by the Hedge Fund, but the effect in this case works its way through the Trading Desk. The quantity sold by the Hedge Fund raises the quantity held by the Trading Desk, increasing its lambda. This in turn leads the Trading Unit to sell into the market, with the end result again being a further drop in prices.

Note that each of the units is acting to maintain stability: the Prime Broker is keeping its loans within bounds given its collateral; the Hedge Fund is maintaining a target level of leverage to control its risk, and the Trading Desk is governing its inventory level through an outflow if its market making activities increases its inventory above a target level. Yet the stabilizing activities at the local level still lead to instability at the global level. This underscores a central point in the functioning of the financial system, namely that it can exhibit global instability even in the face of each unit acting to control its risk.