A. Credit Card Payments on the Internet

- Processing the Transactions

- Problems

- Fraud

- Privacy

- Micropayments

B. Debit Cards on the Internet

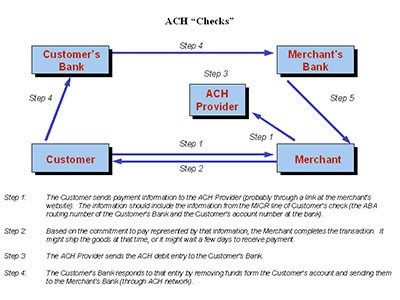

C. ACH Transfers (WEB Entries)

D. Foreign and Cross-Border Payments

Figure 14.1 - ACH "Checks"

E. A Note on Mobile Payments

Problem Set 14

Problem Set 14

14.1. Cliff Janeway (your book-dealer client) comes to see you to talk about developments in his industry. He finds that many of the people from whom he buys books now have many of the items he needs available for sale over the Internet. The three sites that he has examined so far accept both credit cards and debit cards. He has heard a lot about fraudulent transactions on the Internet, and he particularly remembers the press coverage when credit-card numbers were stolen in 2000 from CD Universe. As a result, he is worried that if he starts making such purchases he will expose himself to a significant risk. What do you tell him about his risks of being charged for unauthorized transactions on his credit card? Would it matter if the retailer from whome he made the purchase forced him to enter a PIN or the CVV from the back of his card? Would your advice be any different for his debit card? What if he made the purchase with a WEB entry? Does it make sense that those things should change the outcome? TILA §133; EFTA §§903(5), 909; Regulation E, §205.6; Regulation Z, §226.12.

14.2. Shortly after Cliff leaves, you get a call from your old friend Don Branson, who recently opened a Web site selling a variety of content useful for philosophy professors and graduate students, ranging from analytical outlines of major works, to translations of works in other languages, to sample questions for use in undergraduate philosophy courses. He had a major sale last week of $4,400 to one Quentin Lathrop (or, at least, to someone sending email from [email protected]). As required by his bank, Don's Web page collected Lathrop's credit-card number, billing address, and telephone number. All of those items appear to match information for the holder of the card that was used for the transaction. Also as required by his bank, Don transmitted that information to the bank before completing the transaction, and waited to be sure that the bank had authorized the transaction. Don then sent the purchased information to Lathrop electronically. Don was happy to receive the money from that sale a few days later, because it was by far the largest sale he had ever done.

Things got worse after that. About three weeks later, Don got a call from the bank saying that Lathrop had repudiated the transaction, claiming that he never visited Don's Website or purchased anything there. Don's banker called this morning to tell Don that Don had to return the money from the transaction. Don (a philosopher by trade) is most puzzled. He feels that he did everything he was supposed to, and has already sent the purchased information to Lanthrop. He does not understand what the purpose of having the bank authorize the transaction if he's still liable if something goes wrong. What do you tell him? Would your answers differ if the purchase had been made with a PIN-based debit card? A signature-based debit card? A WEB entry?

14.3. Would your answers to the previous question be different if the purchaser used a cellphone to communicate with and received information from the merchant instead of an Internet connection? Would the EFTA apply? TILA? (Consider both the case where the charges are posted to a credit-card or debit-card account.)

14.4. Your congressional representative, Pamela Herring, asks for your help on a new bill she is developing. She has been trying to update the protections Congress has provided for consumer payment systems. Her perception is that debit cards and credit cards are more or less substitutes for each other. Thus, she wonders whether you think it would be a good idea, at least in the Internet context, to extend the right to withhold payment from TILA §170(a) to the EFTA, so that debit-card Internet purchasers would have the same right to withhold payment as credit-card purchasers do. What do you think?